Location Intelligence Data: What Decision-Makers Need to Know in 2026

Jean-Thomas Rouzin - Reading time : 12 min

Table of contents

If your team cannot name the source of the data behind your store finder, your checkout autocomplete, and your local landing pages, you do not have a location strategy. You have three vendor invoices and an outage waiting to happen. Location intelligence data is the layer that decides whether customers find you, choose you, and finish the cart - and in 2026, the cost, residency, and ownership of that data are board-level questions.

What location intelligence data actually is

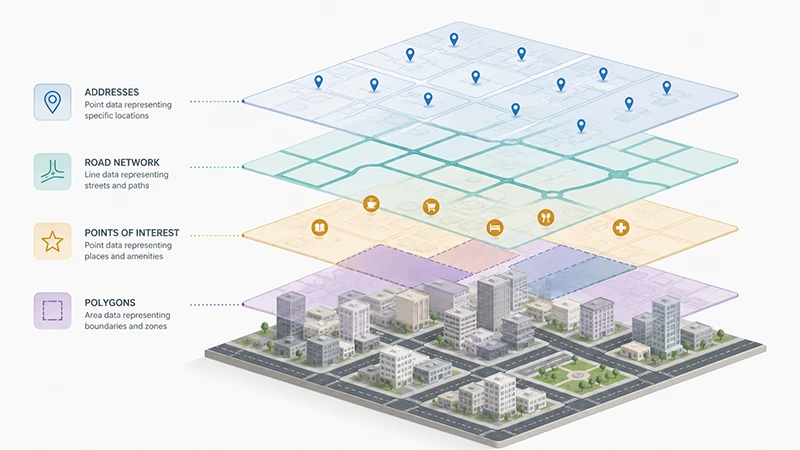

Location intelligence data is the structured spatial information that lets software answer questions like "where is the user," "what is near them," "how long would it take them to get to a store," and "is this address real." It is not one dataset. It is a stack: addresses and postcodes, points of interest, road networks, administrative and custom polygons, travel-time matrices, and the metadata that ties them together (accuracy class, freshness date, source country, licence terms).

Providers like Google Maps Platform, Mapbox, HERE, and TomTom each tune this data for different priorities. Mapbox tunes for in-car navigation and ADAS - its largest customer references are automotive (the Toyota RAV4 partnership, Dash for OEMs). HERE tunes for trucking, weight-aware routing, and EV charge-aware journeys. TomTom builds Orbis Maps for hybrid open/proprietary mobility. Google tunes for consumer discovery on its own apps. None of them tune for retail commerce as a first-class workload. That is why "use Google's data" is rarely the strategic answer for a CMO or CTO who needs spatial context for catalogue, checkout, and local SEO at the same time.

Three forces have pushed location intelligence data out of engineering and into the executive layer in 2026.

Search has fragmented. Google AI Overviews, Perplexity, and ChatGPT answers cite local pages that carry rich spatial context (proximity POIs, neighbourhood, transport, opening hours). Thin store-finder pages no longer rank, and they no longer get cited. Acquisition through local search now depends on the data behind the page, not the page template.

Conversion sits on the address field. Retailers running A/B tests on mobile checkout consistently report double-digit conversion uplift when the multi-field address form is replaced with a one-field autocomplete that returns rooftop-precision results - up to 35% in published case studies (treat as upper bound, not average). The data behind that autocomplete - which postal authority, which freshness, which residency - decides whether the lift is real or a marketing claim.

Pricing has separated from value. Google Maps Platform retired pooled credits after March 2025 and moved to per-SKU, tier-dependent billing. The same map session can cost two or three different amounts depending on which terminator the user hits, and Place Details now ranges from $5 to $20 per 1,000 calls depending on tier. Forecasting a TCO without modelling the data path is no longer possible from a pricing page alone.

None of these are abstract trends. They each map to a line on the next P&L: organic acquisition, mobile cart completion, and infrastructure spend.

The seven types of location intelligence data that matter for commerce

A useful way to break down "location data" before buying anything is by the role each layer plays in the funnel.

Data type

What it is

Where it shows up in the funnel

Quality signal that matters

Addresses

Structured postal addresses with rooftop coordinates

Checkout autocomplete, delivery, invoicing

Postal-authority source, country coverage, ROOFTOP rate

Points of interest (POIs)

Stores, landmarks, transport, services with attributes

Store finder, marketplace listings, local pages

Freshness date, attribute depth, retail-curated vs consumer-curated

Different ICPs lean on different layers. A retail e-commerce site lives or dies on the address layer at checkout and the POI layer for store finders. A marketplace lives on POIs, isochrones, and custom polygons. A logistics platform lives on the road network and matrices. If your provider treats all of these as equally important, they are tuned for someone else.

Build, buy, or license: how decision-makers should frame the choice

Three procurement paths exist for location intelligence data, and they have different five-year cost profiles.

Build (open data + in-house pipeline). Anchor stack is usually OpenStreetMap plus Leaflet or MapLibre, plus a self-hosted geocoder (Nominatim, Pelias). Lowest unit cost at scale, full data residency control, no per-API call charges. Pays for itself only above ~100M monthly requests AND with at least one engineer permanently allocated to data pipeline, quality regression, and update cadence. Most retailers and marketplaces fail the second condition silently - the engineer gets reassigned and the pipeline rots.

Buy (commercial maps platform). Anchor stack is Google Maps Platform, Mapbox, HERE, TomTom, or a regional specialist. Highest unit cost at low volume, lowest engineering overhead, fastest time to value. Lock-in risk varies sharply by provider - Google's terms of service restrict caching and downstream use of geocoding results, and Mapbox has product-specific clauses on Navigation SDK and Dash that include perpetual, sublicensable rights on user inputs (treat the exact wording as something to review with legal before signing).

License (data-only). Anchor model is buying raw datasets (Infobel for European POIs, postal-authority files for UK PAF, government open data for boundaries) and running your own serving layer on top. Useful for retail with strong data engineering and a compliance-sensitive market. Less common as the default path because the serving layer (search, ranking, routing) is the hard part, not the data file.

The decision framework that holds for most commerce decision-makers in 2026 is shorter than vendor decks suggest.

Your situation

Recommended path

< 10M monthly location requests, ≤2 markets, no data sovereignty mandate

Buy. Pick a commercial platform with predictable pricing and a free tier you can prototype in.

10-100M monthly requests, EU customers, retail or marketplace

Buy from a vendor with EU-hosted infrastructure. Validate residency on the provider's /legal page, not on their marketing site.

> 100M monthly requests, full-time spatial team, multi-market

Hybrid: buy for the customer-facing layer (search, autocomplete), license raw POI/address data for the analytical and SEO layers.

Buy from a vendor whose data, hosting, and support team are EU-based. Avoid US-routed APIs at all costs.

Pure open-source preference, no SLA needed (small site, internal tool)

OpenStreetMap + Leaflet. Be honest about who owns data quality regressions.

The trap most teams fall into is choosing "buy" by default from the dominant US platform, then discovering at 50M requests that their unit cost has tripled, their data lives in US infrastructure, and a competing service of the same vendor (Google Hotels, Google Local Services, Google Flights) is bidding against them on the queries their own users generated.

What "good" location intelligence data looks like

Before signing with any provider, four criteria matter more than feature parity.

Source authority. ROOFTOP-level geocoding in the UK should come from Royal Mail PAF or an official equivalent, not from interpolation. In France, premium address data should come from official local providers. A "worldwide" geocoder that quietly downgrades to centroid in countries where you have customers is a liability at checkout. Ask any candidate vendor to name their source per country.

Freshness cadence. POI freshness in retail decays in months, not years. A store finder fed by a POI base last refreshed 18 months ago will direct customers to closed locations and damage your brand more than missing a feature. Ask vendors when each country's data was last refreshed and how that cadence is contracted.

Data residency and lineage. Where is the API call processed, where is the response stored, what does the provider retain. Three different answers, three different contracts. Under GDPR, address data tied to a checkout transaction is personal data; the transfer mechanism matters. For EU customers, the safest answer is end-to-end EU processing. For vendors who route through US infrastructure, ask for a Data Processing Addendum and the standard contractual clauses (SCCs) reference.

Ownership of derived data. When a user types into your address field, who owns the resulting record? Some commercial platforms reserve the right to use that signal to improve their own products and ad ecosystem - the major US platforms in particular include broad usage clauses for telemetry and inputs. A European location intelligence platform should not need that right to deliver service. Verify the answer in writing.

Common pitfalls that cost money quietly

Five mistakes show up repeatedly in post-mortems on location stacks.

Treating the maps API as commodity and the data behind it as free. Maps APIs are a thin interface over data that costs the provider real money to curate; the platform that bills lowest per call is often the one with the thinnest data underneath.

Including Place Details in store-locator cost models. Store data is hosted by the retailer - your own JSON file or database. Place Details is only used to resolve the address the user typed, not the stores you display. Most "store locator TCO" simulations from sales decks inflate this line by 5-10x.

Confusing per-keystroke and session billing. In a modern Google Maps session terminated with Place Details Pro or Enterprise, the autocomplete keystrokes are free. The differentiator versus alternatives is rarely the autocomplete cost itself - it is what happens when the session is abandoned, and whether session tokens are mandatory.

Ignoring contractual restrictions on data reuse. Google's terms forbid caching geocoding results beyond 30 days for most use cases and forbid displaying Google geocoding results on a non-Google map. Most teams discover this at the architecture review, six months in.

Treating "EU-hosted" as a marketing claim. "EU-hosted" should mean every step of the request path stays in the EU, including the support and ops teams. Read the data processing addendum, not the homepage.

Where Woosmap fits in (and where it does not)

Woosmap is the European location intelligence platform behind 220+ enterprise clients across retail, automotive, logistics, travel, hospitality, insurance, and marketplaces. The data layer is curated specifically for commerce use cases - retail POIs, ROOFTOP-precision addresses with worldwide coverage (with premium precision in France and the UK from official local data providers), Distance and Isochrone APIs for travel-time ranking, and a free tier of 10,000 requests per month on most APIs. Enterprise plans include a dedicated Customer Success Manager, health checks, workshops, and budget monitoring; the published Enterprise SLA is 99.9%. Woosmap processes 28B+ location-context calls annually.

Woosmap is not the right fit for in-car turn-by-turn navigation (Mapbox and HERE are tuned for that) or for global consumer discovery in markets like China, Korea, and Japan where it does not cover. It is the right fit when retail-curated commerce data, predictable per-1,000-request pricing, and EU-based engineering and support are decision criteria.

How to choose a location intelligence data partner in 2026

A short checklist that has held for most retail and marketplace selections.

Map your three highest-volume calls. Usually one geocoding, one map load, one distance/isochrone. Get a real quote for those at your real volume from at least three vendors. Compare to your current Google bill at the same volume.

Ask each vendor where the data comes from per country. A vendor who answers fluently usually has nothing to hide. A vendor who routes the question to legal usually has something.

Test residency in the contract. "EU-hosted" lives in the Data Processing Addendum or it does not exist.

Pilot on the lowest-risk surface first. A new geocoder behind a store finder is reversible. A new geocoder behind production checkout is not. Migrate in that order.

Plan the exit before signing the entry. Caching rights, export rights, format portability. If a vendor cannot answer these in writing, the lock-in cost is the real headline price.

Frequently Asked Questions

What is location intelligence data, in plain language?

Location intelligence data is the layered set of spatial information that powers any feature involving where things or people are. The layers most retailers and marketplaces depend on are addresses (for delivery and checkout), points of interest (for store finders and listings), road networks (for delivery promises), and administrative or custom polygons (for service zones). It is not the maps API itself - the API is the interface; location intelligence data is what sits underneath.

How is it different from a Google Maps API?

The maps API is the way your application asks questions. Location intelligence data is the answer the underlying database can give. Two vendors with similar APIs can deliver radically different answers because their data sources, freshness cadence, and country coverage differ. A retail-focused platform like Woosmap and a consumer-discovery platform like Google Maps are both queried similarly; they return different facts about the same address because they curate different sources.

Should we build our own location intelligence stack on OpenStreetMap?

Only if you have a permanent engineering team funded to maintain it. OpenStreetMap, Leaflet, and self-hosted geocoders are economically attractive above ~100M monthly requests, but the hidden cost is the engineering discipline to monitor data quality regressions, refresh imports, and own incidents on Christmas Eve. Most commerce teams that try this path eventually move back to a commercial vendor for the customer-facing layer and keep open data for analytics only.

How does GDPR apply to location intelligence data?

An address entered at checkout, an IP-based location used for content personalisation, and a delivery-tracking coordinate are all personal data under GDPR when tied to an identifiable person. Three things matter for compliance: lawful basis at collection, residency of processing (EU-only is the safest answer for EU customers), and the contractual transfer mechanism if any processing leaves the EU. Vendor terms vary widely; ask for the Data Processing Addendum, not the marketing page. Reference: EU GDPR Article 44 on transfers.

What does Mapbox's automotive focus mean for retailers?

Mapbox is a strong product, but its roadmap is centred on automotive use cases - the Navigation SDK, Dash App, ADAS SDK, and OEM partnerships like the Toyota RAV4 integration. The data and tooling are tuned for in-vehicle journeys. For a marketplace ranking listings by travel time at city scale, or for a retailer running a store finder at checkout, that tuning is not the priority. It is not that Mapbox cannot serve those use cases - it is that the roadmap is optimising elsewhere.

How much does location intelligence data cost?

Pricing is per 1,000 requests on most commercial platforms, with a free tier (Woosmap's is 10,000 requests per month on most APIs, 5,000 for Place Details and Traffic; Google retired its pooled credits after March 2025). A common reference point in 2026 is that a retail or marketplace workload running on a European commerce-tuned platform costs around 40-50% of the equivalent Google Maps Platform Pro tier bill at the same usage. Validate with a real quote on your real volume before committing.

What is the single biggest cost mistake decision-makers make on location data?

Forecasting the bill from the pricing page without modelling the call pattern. Place Details billing tiers, session-token mechanics, and per-tile versus per-load distinctions can move a TCO estimate by 2-3x without changing user-visible behaviour. The fix is to instrument current call volumes for one month before requesting quotes - "we use Google Maps" is not a brief, "we make 18M map loads, 4M autocomplete sessions, and 600k geocodes per month, 70% in the EU" is.

Where to go next

If you are pricing a migration: model your own load against the comparison in our Google Maps API alternatives breakdown - it is the buyer-side companion to this strategic primer.

This guide was written byJean-Thomas Rouzin, CEO of Woosmap. Jean-Thomas leads a European location intelligence platform serving 220+ enterprise clients across retail, logistics, and travel, processing 28B+ location context calls per year with a 99.9% SLA on the Enterprise plan.