Geospatial and Location Intelligence: A Decision-Maker's Guide for 2026

Jean-Thomas Rouzin - Reading time : 11 min

Table of contents

Geospatial and location intelligence get treated as one category, but they describe two different layers. Geospatial is the discipline of working with spatial data - coordinates, road networks, polygons, points of interest. Location intelligence is the API and SDK layer that turns that data into live commerce outcomes: ranking, search, autocomplete, distance. Confusing the two costs procurement money.

The vocabulary problem decision-makers inherit

Picking the wrong location stack costs a typical European retailer up to 40 to 70 percent of its location bill and leaves search rankings exposed to vendors who tune their data for other industries. The conversation usually goes wrong before procurement starts, because the two terms get used as if they meant the same thing. They do not. One is the underlying discipline. The other is the commercial application layer. Confusing them is how you end up paying for a GIS platform when you needed a checkout autocomplete, or wiring a navigation SDK into a store finder it was never optimised for.

Vendors pitch "geospatial and location intelligence" as a single category because it inflates the addressable market. Inside that label sit four very different product worlds: desktop GIS (Esri, QGIS, CARTO), consumer maps (Google Maps Platform), automotive and navigation (Mapbox, HERE Technologies, TomTom), and commerce-grade location platforms (Woosmap and a handful of regional peers). Each of them processes spatial data, so each of them can answer "yes" when a buyer asks if they do geospatial and location intelligence. The procurement question is which of those worlds matches your business problem - and the honest answer is rarely "all of them."

What geospatial actually means

Geospatial is the science and engineering of working with data that has a location attached. The raw materials are spatial coordinates (latitudes, longitudes, projections), vector geometries (points, lines, polygons), raster layers (aerial imagery, terrain, satellite), road networks, and the metadata that ties them together (accuracy, freshness, source country, licence terms). The discipline standardises on formats and protocols maintained by bodies like the Open Geospatial Consortium - WMS, WFS, WMTS, GeoJSON, and the OGC API family.

Geospatial tooling lives close to those raw materials. A GIS specialist uses it to build catchment-area models, analyse network coverage, draw isochrones for trade-area planning, run spatial joins for site selection, or publish thematic maps. The user is typically a data analyst, a planner, or a GIS engineer working inside the business, not an end-user buying shoes on a mobile checkout. The deliverable is often a report, a dashboard, or a one-off model, not a millisecond-latency API call wired into a live commerce funnel.

Geospatial as a discipline is decades old, deeply standardised, and largely vendor-neutral at the format layer. Where vendors differentiate is on data quality, processing scale, and the developer experience of putting that data to work.

What location intelligence means in a commercial stack

Location intelligence is the layer that turns spatial data into business outcomes - acquisition, engagement, conversion - inside live customer-facing software. It is the difference between a static catchment-area study and an address autocomplete field that recovers a cart, a store-finder page that ranks first on a city search, or a delivery slot that reflects the actual travel time from a fulfilment node.

The capabilities a commerce-grade location intelligence platform exposes through APIs and SDKs typically include:

Address autocomplete with ROOFTOP geocoding precision and worldwide coverage.

Reverse geocoding (turn a coordinate back into a usable address).

Place search and detail lookups for points of interest like stores, restaurants, or pickup lockers.

Distance, route, and isochrone calculations across driving, cycling, walking, and transit modes.

Map rendering as either vector tiles, static images, or embedded widgets.

Geofencing and location-aware push notifications through mobile SDKs.

A geolocation lookup (IP based, no personal data collected) for region detection.

The user here is not the analyst. It is the customer in front of a checkout, a CRM journey trigger, a local landing page that needs to rank for a city query, or a marketplace search box that has to interpret "near Liverpool Street" and order results by realistic travel time. Latency matters. Coverage matters. Data privacy and security posture matters. Pricing predictability matters because the API gets called millions of times a month, not once for a quarterly report.

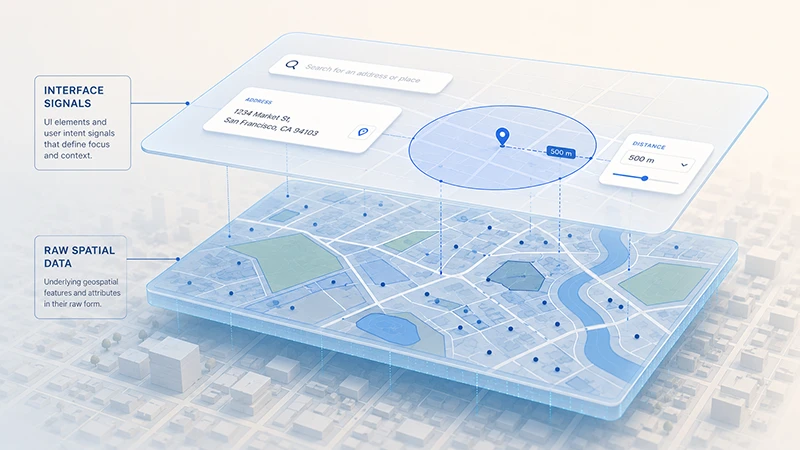

How geospatial and location intelligence connect

A useful way to picture the connection is two stacked layers. The lower layer is geospatial - raw addresses, road networks, polygons, POIs, accuracy classes, licence terms. The upper layer is location intelligence - the APIs, SDKs, search engines, and widgets that consume that data and answer specific commercial questions in milliseconds.

A commerce-grade platform owns or licenses high-quality geospatial assets and then engineers the location intelligence layer on top. A pure GIS vendor stops at the lower layer and hands you toolkits to do your own analysis. A consumer maps platform like Google Maps Platform owns enormous geospatial assets but tunes its surface for consumer discovery on its own apps, not for retailers wiring conversion funnels. Automotive-first vendors tune their geospatial data and routing engines for in-car navigation and ADAS, and their commercial terms reflect that focus.

You will see the same providers competing across both layers, but the strategic question is which layer is doing the heavy lifting in your business case. If you need cohort analytics on store performance, you are buying geospatial analysis. If you need to lift add-to-cart and recover address-entry conversion, you are buying location intelligence. Most retailers eventually need a little of both, but the entry point decides which vendor archetype you should be talking to first.

Heavy licensing for runtime API workloads; no commerce primitives

Consumer maps (Google Maps Platform)

Mixed (developers + end-users)

Consumer discovery on Google surfaces; per-load pricing

Pricing scales with end-user volume; data flow through US infrastructure raises EU residency questions

Automotive and navigation (Mapbox, HERE, TomTom)

Carmakers, navigation apps

In-car maps, truck routing, EV charge-aware journeys, ADAS

Roadmap not optimising for retail commerce checkout flows; data licence terms tuned to navigation, not e-commerce

Commerce location platforms (Woosmap and regional peers)

Retail, marketplaces, hospitality

Local SEO, store search, address autocomplete, distance sorting

Lighter for hardcore desktop GIS analytics; pairs with a GIS partner if needed

The point of this table is not to declare a winner. It is to make the trade-off explicit before the procurement RFP rather than during the migration two years later. Mapbox has navigation primitives for automotive use cases - the Toyota RAV4 ADAS partnership and Dash for OEMs are public evidence of where its roadmap points. HERE Technologies leads on deep truck routing (weight, width, hazmat) and EV-aware journeys. TomTom builds Orbis Maps for hybrid open and proprietary mobility data. None of these are wrong - they are just optimised for someone who is not selling shoes online.

How to evaluate a location intelligence platform

For a decision-maker comparing vendors, five practical criteria separate marketing language from operational fit.

Your situation

What to verify

Why it matters

EU-headquartered retailer

Data residency, hosting region, US data transfer posture

Routes API calls through US infrastructure can trigger GDPR Article 44 transfer questions; ask for documented EU-hosted infrastructure

A poorly priced autocomplete inflates checkout cost per session; verify whether the vendor charges per keystroke or per completed session

Local SEO leverage

Quality of POI and address data, freshness cadence, spatial signals for landing pages

AI answer engines cite local pages with strong spatial context; weak data weakens organic acquisition

Marketplace search relevance

Hybrid text + geo search, distance versus travel-time sorting, polygon-aware filters

Straight-line distance sorting buries the right result in dense cities; you need travel-time aware ranking

Predictable cost at growth

Pricing model (per request versus credits), price increase history, enterprise SLA terms

Some vendors have a documented pattern of regular price increases; budget the next renewal cycle, not the current invoice

The questions are deliberately written so they cannot be answered with a slide. They require the vendor to point at documentation, contract clauses, or a sandbox account.

The cost dimension without the slogans

A common executive shortcut is "are you cheaper than Google?" That question hides the real one, which is "does my workload match what Google Maps Platform charges for?" Google prices its mapping product per map load and prices session-terminated autocomplete at zero for Pro and Enterprise tiers, but per-request for Essentials. Place Details remains paid in every tier. Once a retailer maps its actual API mix - autocomplete, geocoding, distance, map loads, place details - the question shifts from "cheaper" to "more value at the same budget."

European commerce-tuned providers commonly position around 40 to 50 percent of Google Maps Platform pricing at the Pro tier for equivalent SKUs, with bigger gaps at scale and tighter parity on autocomplete (both can be free in modern session models). Treat any single-number cost claim with caution and ask for a calculation against your own monthly volumes. A free tier of 10,000 requests per month is industry-standard for most APIs and should not be the deciding factor - the deciding factor is what happens at the third decimal place when volumes go past one million.

Where do API calls hit infrastructure first, and is there a documented EU-hosted path? This is a data privacy and security question - residency posture protects regulatory exposure, while hosting topology protects against shadow profiling of your customer base by a vendor with adjacent ad or commerce interests.

What does the vendor's terms of service say about retention, caching, and downstream usage of geocoding results? Some major vendors restrict caching and prohibit displaying their geocoding results on non-vendor maps. Some product terms - notably navigation-focused SDKs from certain providers - grant the vendor a perpetual, transferable licence on user inputs, and these clauses warrant a legal review before signing.

These are not theoretical risks. They show up in renewal negotiations, regulatory audits, and board-level conversations about whether the retailer's location data is being used to train a competing ecosystem.

When you actually need GIS, location intelligence, or both

Three lightweight rules cover most situations a CMO, CTO, or CPO will face in 2026.

You probably need a GIS tool, not a location intelligence platform, when your primary deliverable is an internal analysis (catchment study, network rationalisation, site selection, demographic modelling). The output is a report or a dashboard, the user is internal, and the latency budget is hours or days. Esri or CARTO is the sensible conversation here.

You probably need a location intelligence platform, not a GIS, when your primary deliverable is a live customer-facing experience that depends on spatial answers in milliseconds. Address autocomplete at checkout, store-finder pages that need to rank, marketplace search ordered by travel time, geofenced re-engagement campaigns. The output is a user action, the user is your customer, and the latency budget is single-digit milliseconds at the ninety-ninth percentile.

You probably need both when your roadmap pairs internal planning (where to open the next dark store) with a customer-facing surface (how to display the next dark store on a checkout flow). In that case, pick the commerce-grade platform first - it touches revenue - and add a GIS partner for the analysis workload.

Frequently Asked Questions

Is location intelligence the same as a GIS?

No. A GIS is a software environment for spatial analysis, typically used by internal specialists to produce reports, models, and thematic maps. Location intelligence is the API and SDK layer that puts spatial answers into live customer-facing software. They share underlying geospatial data, but their users, latency budgets, and commercial models are different.

Why are vendors pitching "geospatial and location intelligence" as one thing?

Because the label expands the addressable market. A GIS vendor wants to sell into a retailer's e-commerce stack; a consumer maps vendor wants to sell into a marketplace's search box; an automotive vendor wants to sell into retail. They are all legitimate products, but they are tuned for different priorities. Buyers benefit from forcing the distinction earlier in the conversation.

How do AI answer engines change the location intelligence question for acquisition?

Google AI Overviews, Perplexity, and ChatGPT cite local pages that carry rich spatial context - proximity points of interest, neighbourhood, transport, opening hours, opening data freshness. Thin store-finder pages are losing both organic ranking and AI citation share. The data behind a local page, not the template, decides whether it gets cited.

What is the right pricing question to ask a vendor?

Not "are you cheaper than Google" - the right question is "model my monthly API mix against your published pricing and show me what scales linearly versus what scales as a step function." A vendor that cannot do that exercise in a sandbox account in 48 hours is either pricing non-publicly or hiding a complexity that will surface later.

Does location intelligence touch GDPR even if no personal data is sent?

Yes. Two angles. First, IP-based geolocation lookups can fall under GDPR depending on jurisdictional interpretation - choose providers that document a no-personal-data posture. Second, address autocomplete and reverse geocoding handle inputs that are personal data, so the residency and retention terms of the provider matter for the data privacy and security posture of the entire checkout funnel.

Can a single vendor cover both automotive and retail use cases well?

Sometimes, but rarely without trade-offs. Automotive-tuned vendors optimise their roadmap, data refresh cadence, and SLAs for in-car experiences. Retail-tuned vendors optimise for catalogue, checkout, and local SEO. The honest answer for most multi-line businesses is to pick two best-of-breed vendors rather than one compromise.

Where to take this next

If you want to go deeper on the buyer-side comparison across the major maps providers, the Google Maps API alternatives breakdown walks through how the leading platforms stack up on capability, pricing model, and commerce fit. For the data layer specifically - what types of spatial data matter, how to source them, and how to avoid vendor lock-in - the location intelligence data buyer's guide goes one level deeper. Developers leading the implementation conversation will get more value from the Mapbox alternatives breakdown and the HERE Technologies alternatives breakdown, both of which sit in the same pillar.

If you are ready to model your own workload against a commerce-tuned platform, Woosmap operates a European location infrastructure built for retail, marketplaces, and hospitality - 220+ enterprise clients, 28 billion location context calls processed annually, 99.9 percent Enterprise SLA, and a free usage tier available across all APIs. To walk through what your monthly API mix would look like at a real commerce volume curve, talk to our team.

The category will keep blurring at the marketing layer. The procurement decision does not have to.

This guide was written byJean-Thomas Rouzin, CEO of Woosmap. Jean-Thomas leads a European location intelligence platform serving 220+ enterprise clients across retail, logistics, and travel, processing 28B+ location context calls per year with a 99.9% SLA on the Enterprise plan.